Planning your exit from government service? Don’t let unnecessary delays steal your peace of mind.

If you’re a South African government employee and you’re getting close to retiring or resigning, there’s one thing most people don’t talk about—but it can make or break your transition:

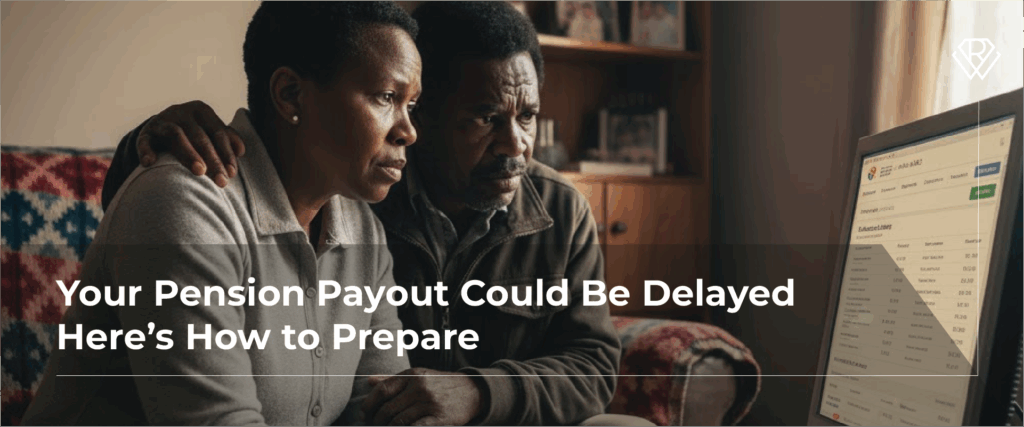

👉 Pension payout delays.

You’ve given years—possibly decades—of your life in service. You deserve a smooth, stress-free exit. But what happens when your lump sum or income is delayed for weeks or even months? For many, it leads to sleepless nights, financial panic, and scrambling for emergency loans.

In this article, we’ll walk you through a real story—and share 5 practical steps to prepare for possible payout delays so you can avoid unnecessary financial stress.

Susan’s Story: The Hidden Risk Most Don’t See Coming

Susan, a long-serving government employee, planned her resignation carefully. She had her paperwork in order and consulted with a trusted advisor.

But despite her preparation, a delay in her pension payout left her financially vulnerable.

She found herself struggling to cover bills—feeling out of control for the first time in her life.

Her story is more common than you think. And that’s why we’re sharing these five key strategies so you can prepare better.

1. Start Planning 12 Months Before You Exit

It used to be okay to start 3–6 months before your exit.

But these days, with changing pension processes and potential formula updates, 12 months is the new gold standard.

Here’s what you should begin doing a year in advance:

- Confirm your preferred exit route: retirement or resignation.

- Request all necessary documentation from your HR.

- Begin your consultation with a specialist who understands GEPF rules.

- Track paperwork submissions and avoid last-minute chaos.

Pro tip: Submitting your documentation early—even a few months before your last working day—gives you time to fix any HR or pension fund errors while you’re still employed.

2. Save Money Before You Exit—Starting with Your Birthday Bonus

The fastest way to build a financial cushion?

🎉 Use your birthday bonus.

This once-a-year double salary can act as your emergency fund. Saving even one month’s salary now could tide you over in case of delays.

Imagine:

- Keeping up with debit orders

- Paying your utility bills

- Avoiding expensive loans

- Staying calm and in control

Your birthday bonus is the perfect tool for this—if you don’t spend it.

3. Save in the Right Place: Easy Access Over High Returns

You might be tempted to invest your emergency money—but that can backfire.

Instead, choose safe and accessible bank products, such as:

- A standard savings account

- A 32-day notice account

- A short-term fixed deposit

Why?

Because you need liquidity, not returns. Investment platforms may offer higher yields, but they can also come with:

- Market risk

- Penalty fees for early withdrawals

- Delays in accessing funds

Keep it simple. In this case, interest earned is less important than access and peace of mind.

4. Review (and Reduce) Your Expenses Before You Leave

Retirement or resignation marks a major lifestyle shift. And your expenses should shift too.

Take a look at:

- Insurance premiums (e.g., disability cover that may no longer apply)

- Subscriptions and services you no longer need

- Monthly spending habits

Ask yourself:

- Do I still need this?

- Is there a lower-cost alternative?

- What can I cut without affecting my quality of life?

The goal isn’t to deprive yourself—it’s to buy yourself time and breathing room while your pension processes.

5. Build a 3–6 Month Emergency Fund—Call It a Peace-of-Mind Fund

Aim to save three to six months of your monthly expenses before you exit.

This will protect you against:

- Pension payout delays

- Tax planning hold-ups

- Processing bottlenecks at HR or GEPF

- Seasonal slowdowns (e.g., December–January holidays)

It’s not just an emergency fund.

It’s your freedom fund.

Because when you have 3–6 months of backup money, you won’t be forced to rush decisions or settle for poor advice under pressure.

Why This Matters: One Chance to Get It Right

When it comes to your pension and income planning, you only get one shot.

If you make the wrong decision or rush your process, it could cost you:

- Tens of thousands in unnecessary tax

- Weeks or months of financial instability

- Lifelong regret

The more you plan, the more freedom you create.

🎥 Watch the full video on YouTube where Dhevan shares Susan’s story and the 5 steps in more detail:

👉 https://youtu.be/v4wNsm-oLQk

Final Thoughts

Don’t let delays steal the joy from your well-earned retirement.

Start early. Save intentionally. Prepare with a partner who understands your unique needs as a government employee.

You’ve done the hard work.

Now let’s make sure your exit is smooth, stress-free, and on your terms.

Need Help Navigating Your Exit from Government?

✅ Watch the free Retire vs Resign Masterclass for government employees

👉 https://www.retirevsresign.co.za/online/

🎟️ Join the in-person Retire vs Resign Masterclass at Durban ICC

🗓️ 1 November 2025

📍 Reserve your seat today: https://www.retirevsresign.co.za/live

🔒 Book a private 1-on-1 consultation for your exit planning

👉 https://www.retirevsresign.co.za/consult/

Disclaimers

• Retirement Wellness SA is an Authorised Financial Services Provider (FSP 31609). This article provides general information and is not direct financial advice.